It finally happened – 7 years out of college and I am finally getting my first 401k match! I’ve dreamed of this moment for so long (yes, I have weird dreams – deal with it). While working at all of my previous jobs, I never qualified for the 401(k) match (if they even had one). If they did have one, you were not eligible for it until you had been there 4 or so years, which is basically unheard of in ad agencies. Well played HR. Well played. Continue reading “My First 401(k) Match, An Updated Salary and Inching Closer to Early Retirement”

It’s time to bring out my planning materials! *rubs hands together maniacally*

It’s time to bring out my planning materials! *rubs hands together maniacally* It’s that time again: Dividend Season! I look forward to it like I imagine people look forward to Christmas, but this happens 4 times a year! Let’s see how we made out this quarter. I received $881.27, which is awesome. That’s 42% more than last year! Since I started investing in 2014 I’ve received $7,380.32 in dividends – that’s almost a full month of my current salary without having to work that’s just dropped into my lap. Insanity! Let’s see if we can top that next quarter (Spoiler: I think we can 😉 ).

It’s that time again: Dividend Season! I look forward to it like I imagine people look forward to Christmas, but this happens 4 times a year! Let’s see how we made out this quarter. I received $881.27, which is awesome. That’s 42% more than last year! Since I started investing in 2014 I’ve received $7,380.32 in dividends – that’s almost a full month of my current salary without having to work that’s just dropped into my lap. Insanity! Let’s see if we can top that next quarter (Spoiler: I think we can 😉 ).

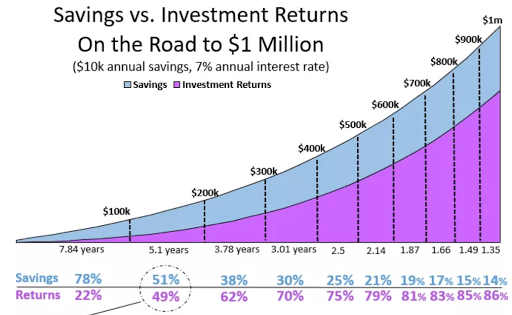

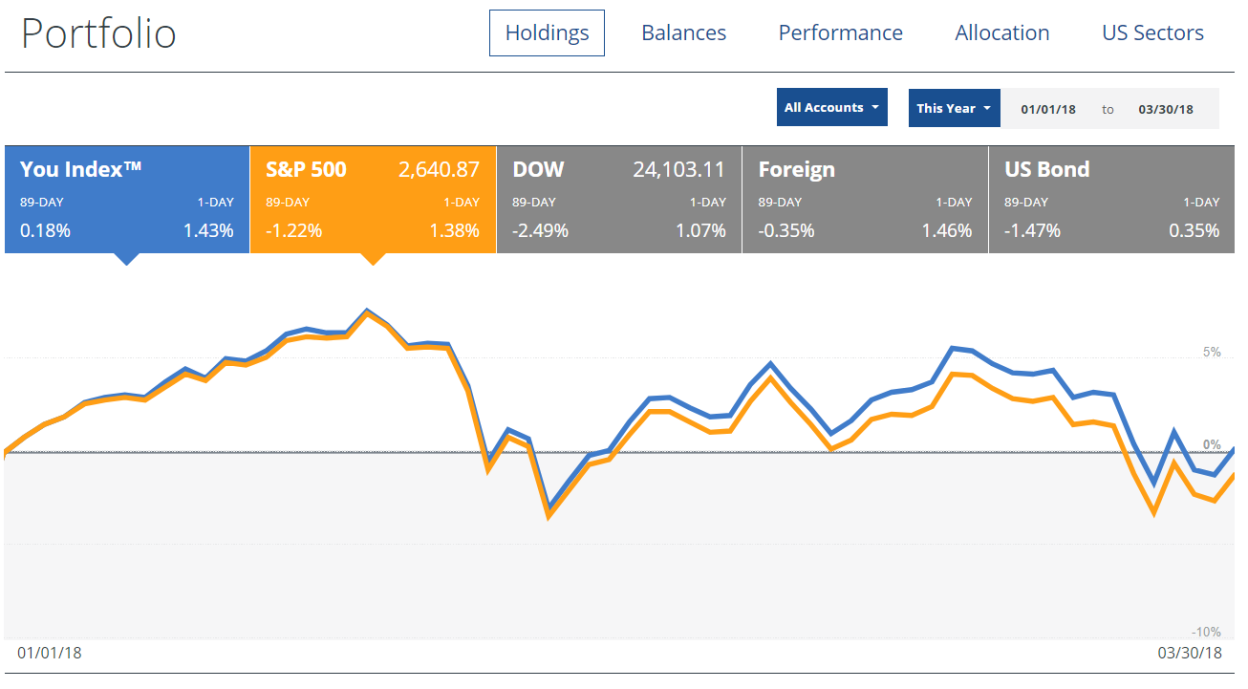

The end of Q1 2018 has me at about 0% market gains for the year (while the S&P 500 is down -1.22%). This inspired me to do a thought experiment. What if the highly improbable happened and the market remains stagnant at a 0% gain until I retire? How long would that add to my working career? My initial thought was several years since the average of 7% would add $17,850 to my current portfolio so my savings for the year would be made of approximately 20% gains and 80% savings.

The end of Q1 2018 has me at about 0% market gains for the year (while the S&P 500 is down -1.22%). This inspired me to do a thought experiment. What if the highly improbable happened and the market remains stagnant at a 0% gain until I retire? How long would that add to my working career? My initial thought was several years since the average of 7% would add $17,850 to my current portfolio so my savings for the year would be made of approximately 20% gains and 80% savings.  It’s the end of Q1, which means it’s once again DIVIDEND SEASON! I look forward to it every 3 months because even though I know this is a distribution from the 3,000+ businesses I partially own it still feels like it’s free money that’s dropped into my account.

It’s the end of Q1, which means it’s once again DIVIDEND SEASON! I look forward to it every 3 months because even though I know this is a distribution from the 3,000+ businesses I partially own it still feels like it’s free money that’s dropped into my account. One of my favorite bloggers GoCurryCracker has a wonderful article on

One of my favorite bloggers GoCurryCracker has a wonderful article on