This is a continuation of my monthly series that records what’s happening in my final stretch to early retirement. If you’re interested in previous posts, they’re here.

I’m not one to bury the lede so: We’re doing this people! Thank you so much for all of your comments on my last post about this decision. I really appreciate all of your encouragement, concerns and advice. After careful consideration it’s been decided: I’m leaving my job in September 2020. Continue reading “It’s Official: I’m Quitting My Job In 10 Months. Here’s The Plan!”

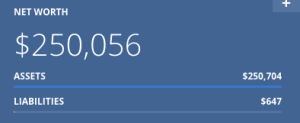

This milestone feels weird to me and I’m not sure why. In January of this year I quickly hit $250,000 net worth thanks to a crazy market, which then entered a correction. It’s taken a few months to get back to where I was now. After adding in my latest paychecks and the market being up 3% we have arrived here.

This milestone feels weird to me and I’m not sure why. In January of this year I quickly hit $250,000 net worth thanks to a crazy market, which then entered a correction. It’s taken a few months to get back to where I was now. After adding in my latest paychecks and the market being up 3% we have arrived here.

As part of my many retirement charts I’ve created one that shows visually how much I’ve saved in $10,000 increments. The market is already going gangbusters in 2018 (though who knows how long it will last) and as a result without any paycheck I have more than $250,000. Originally I was just excited to fill in another bubble on my visual net worth sheet and enthralled by the fun of thinking about having “a quarter of a million,” but I just realized something: $250,000 is half of what I need to retire. I’m halfway there! That’s crazy! And based on the magic of compound interest my money will keep working for me and start earning money faster than I can. It looks like I’m halfway to retirement money-wise and less than halfway in regards to time: 2 years and 11 months to go!

As part of my many retirement charts I’ve created one that shows visually how much I’ve saved in $10,000 increments. The market is already going gangbusters in 2018 (though who knows how long it will last) and as a result without any paycheck I have more than $250,000. Originally I was just excited to fill in another bubble on my visual net worth sheet and enthralled by the fun of thinking about having “a quarter of a million,” but I just realized something: $250,000 is half of what I need to retire. I’m halfway there! That’s crazy! And based on the magic of compound interest my money will keep working for me and start earning money faster than I can. It looks like I’m halfway to retirement money-wise and less than halfway in regards to time: 2 years and 11 months to go! This year I had more than just monetary goals. They were:

This year I had more than just monetary goals. They were: