As an exercise I wanted to make sure that my retirement budget of $20,000 could include my current spending and items I need to add in retirement, which I’ll detail below. I’m happy to report that it’s looking really good! Let’s see what’s inside: Continue reading “Projected Retirement Budget”

Category: Finance

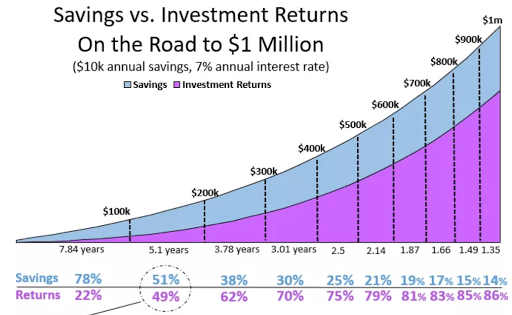

Market Noise > Contributions

This graph was made by the lovely Four Pillar Freedom.

We’ve reached the threshold. My monthly contributions to my investments are almost completely obscured by the market noise. I now add 2% of my current net worth to my investments each month and recent daily fluctuations have been more than that: Down 2.5%, Up 2% etc. I think I’ve reached what a new favorite blogger of mine Four Pillar Freedom describes as the point when the market makes a bigger impact than your contributions. Continue reading “Market Noise > Contributions”

A Minimum Wage Employee By My Side

I just realized that my passive income from investments (assuming an average 7% market return) has now surpassed what a minimum wage employee would make working 40 hours a week, 52 weeks a year. WOWZA! At the beginning of 2018 I had $237,000, which would generate $16,590 at 7% while a minimum wage employee would receive $15,080. That’s wild!

I have an invisible minimum wage employee working hella hard while I sleep, away from my day job, which I think is a very cool idea. I’ve touched on this phenomenon in a previous post, but she was just a teenager working part time after school then. Now she’s a full-timer. This just got serious!

Now we should probably working on raising that minimum wage (Washington did recently) so the average isn’t so low!

A Flat Market = No Problem

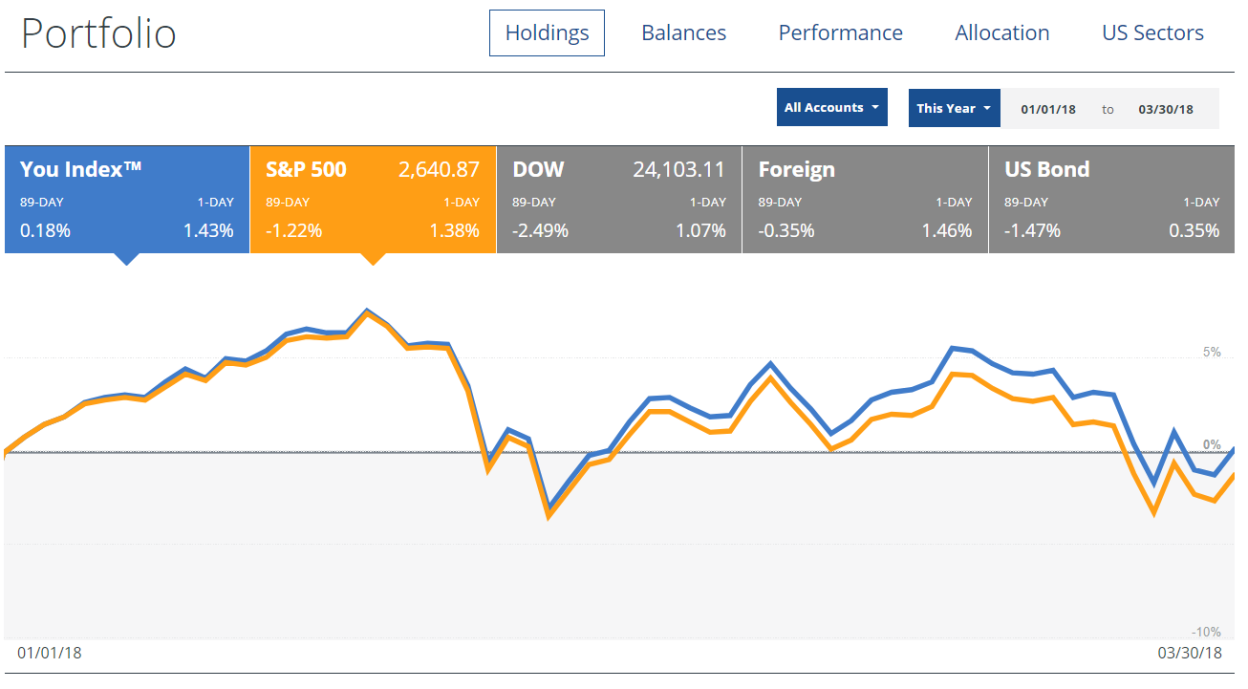

The end of Q1 2018 has me at about 0% market gains for the year (while the S&P 500 is down -1.22%). This inspired me to do a thought experiment. What if the highly improbable happened and the market remains stagnant at a 0% gain until I retire? How long would that add to my working career? My initial thought was several years since the average of 7% would add $17,850 to my current portfolio so my savings for the year would be made of approximately 20% gains and 80% savings. Continue reading “A Flat Market = No Problem”

The end of Q1 2018 has me at about 0% market gains for the year (while the S&P 500 is down -1.22%). This inspired me to do a thought experiment. What if the highly improbable happened and the market remains stagnant at a 0% gain until I retire? How long would that add to my working career? My initial thought was several years since the average of 7% would add $17,850 to my current portfolio so my savings for the year would be made of approximately 20% gains and 80% savings. Continue reading “A Flat Market = No Problem”

Sweet Sweet Dividends

It’s the end of Q1, which means it’s once again DIVIDEND SEASON! I look forward to it every 3 months because even though I know this is a distribution from the 3,000+ businesses I partially own it still feels like it’s free money that’s dropped into my account.

It’s the end of Q1, which means it’s once again DIVIDEND SEASON! I look forward to it every 3 months because even though I know this is a distribution from the 3,000+ businesses I partially own it still feels like it’s free money that’s dropped into my account.

So how did I make out this quarter? Like a bandit if I do say so myself! I made $787.04 from my investments. That’s a 43% increase from last year! Yes my investments have increased 56%, but that’s besides the point 🙂 . Just assuming an overall 43% increase from last year’s dividends of (even though it will be more) I’ll receive $3,916.04 in dividends in 2018. Woah. That’s like 2 weeks of salary! And I’ll receive it no matter what the market does (we’re down 1% for the year at the time I write this). An extra half a month’s salary no matter what. I like the sound of that. To next quarter!

Q1 Budget Check-In 2018

I understand that time moves faster the older you get, but HOW is the year 25% done?! I feel like it’s crawling and then look at the date and feel like it’s flying by. Fascinating. I wanted to check in on my goal to decrease my spending from $18,436.60 last year by $436.60 to a solid $18,000 this year. Let’s see how it’s going.

Exposure Therapy

One of my favorite bloggers GoCurryCracker has a wonderful article on Exposure Therapy. He basically gives advice that is contrary to a lot of other finance bloggers who say ignore the stock market completely (which I would argue is a little impossible in our tech heavy, media heavy world). GoCurryCracker suggests that yes we should ignore it as in not change our plans based on it, but that we should also pay attention when it drops so we can see how we feel ‘losing’ money.

One of my favorite bloggers GoCurryCracker has a wonderful article on Exposure Therapy. He basically gives advice that is contrary to a lot of other finance bloggers who say ignore the stock market completely (which I would argue is a little impossible in our tech heavy, media heavy world). GoCurryCracker suggests that yes we should ignore it as in not change our plans based on it, but that we should also pay attention when it drops so we can see how we feel ‘losing’ money.800 Credit Score

Well that happened. Apparently I now have a 800 credit score according to Equifax (not that I trust them at all – so many breaches. Goodness people). Nevertheless it’s fun to see and hilarious since I’m such a credit card churner. An 800 credit score with an average credit card age of less than 2 years 🙂 . It’s possible. To 850!

Well that happened. Apparently I now have a 800 credit score according to Equifax (not that I trust them at all – so many breaches. Goodness people). Nevertheless it’s fun to see and hilarious since I’m such a credit card churner. An 800 credit score with an average credit card age of less than 2 years 🙂 . It’s possible. To 850!