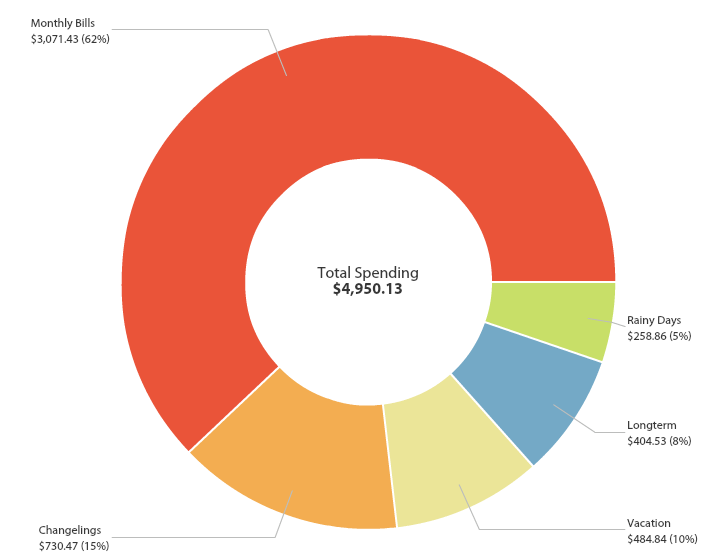

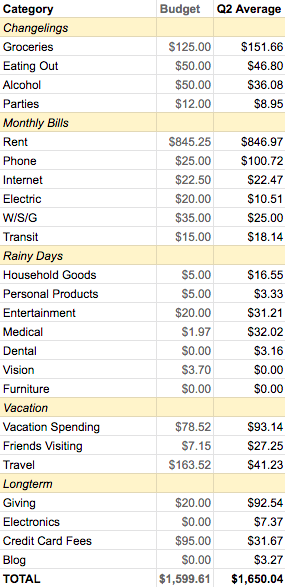

Sooo can someone tell me where half of 2019 went? Apparently it’s 50% over, which means it’s time for another quarterly budget review! Above is a snapshot of my Q2 spending from YNAB. Let’s get into the nitty-gritty:

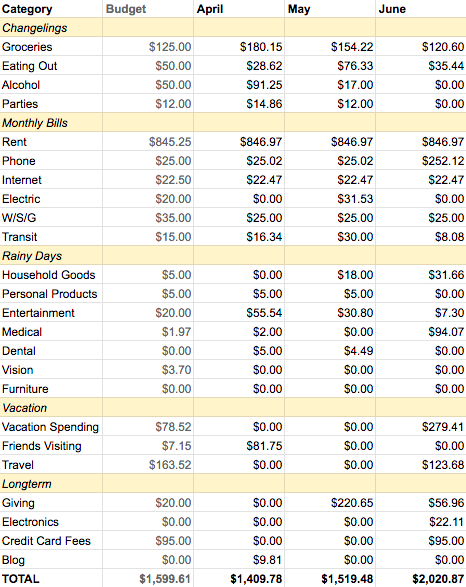

And for a month by month breakdown:

CHANGELINGS – $243/MONTH

I call this section “changelings” because they’re the items that change the most month to month.

Groceries – $151.66/month

I was a little over on groceries this quarter, but I’ve been eating a lot of delicious fruit and have no regrets! We’ve also been experimenting with new dishes, such as fajitas where we use our awesome Sous Vide machine to make the steak perfectly tender and have tried both using our crockpot and stir frying the veggies to get them to ideal crispiness. I prefer the crockpot method while my partner prefers stir frying.

For more info on how I eat like a queen while maintaining a low food budget and eating a lot of meat on keto check out my post here that details what I bought in a month and the kinds of food I made from it.

Eating Out – $46.80/month

I’ve been on point with my eating out budget despite the fact that we went to a fancy Brazilian steakhouse in May. I think those places might be a racket because they’re super expensive (even with a Groupon…) and the unlimited and delicious meat they offer filled me up surprisingly fast despite me training for it (and by training I mean not eating breakfast…) In other news, this eating out spending also included me FINALLY finishing up that Chipotle Gift Card that I got from cashing in unwanted United points.

Alcohol – $36.08/month

You might notice that my alcohol spending for June was $0. I’ve decided to take a 100 day break from alcohol. Dry January turned into a Wet February so I decided to shake things up further. After January I still found myself turning to a glass of wine to unwind after a stressful workday and I don’t want that to be my default. I’m happy to say that I’m almost 50 days into this self-imposed challenge and have been loving it! I even made it through my work ‘hell month’ without daydreaming about sipping a chilled pinot grigio after the work day was done.

As a result of this challenge, we’ve been buying more fancy non-alcoholic drinks like seltzer (which probably also contributed to my increased grocery spending). So fancy! This has had the added benefit of giving me ‘guns’ from lugging 12 packs of seltzer up our hill *Welcome to the gun show!*

MONTHLY BILLS – $1,023/MONTH

Pretty self-explanatory. This section doesn’t vary a lot month to month.

A stand out expense this quarter is my larger than usual phone bill in June. I’ve been a happy Republic Wireless customer for over 4 years now because of their awesome service and low prices. This spring they introduced a new way to save money: Annual Plans.

Previously all plans were month to month, but they started offering an annual plan that takes 2 months off your 12 month bill so of course I switched over, which was as easy as clicking a button. I’m looking forward to seeing my phone bill category report $0 for a full year!

RAINY DAYS – $86/MONTH

This section is named based on a principal in YNAB: saving a little for inevitable things that don’t happen monthly so when a rainy day hits you have the funds.

Household Goods – $16.55/month

This quarter, rainy day purchases included a new non-stick pan, which is basically magic. I used to hate making eggs because I would have to soak the pan all day or strain my arms to get the residue off the pan. Instead I can clean this pan with a swipe of my sponge. Buying one a few years ago was a sensational and timely purchase since becoming keto 2.5 years ago has made me egg obsessed. We also purchased a new plunger (people don’t call my blog “brutally transparent” for nothing…)

Medical – $32.02/month

This included a $10 co-pay for a shockingly amazing medical experience that I’ll talk about in another post (it’s shocking because I live in well…America). To give you the highlights, I also paid $80 for medicine – half of which I needed and half of which I did not. I guess I’ll be asking more questions at the pharmacy next time. My cheapskate self from this embarrassing incident temporarily disappeared. Or maybe I was just caught off guard by how surprisingly awesome my medical experience was.

Entertainment – $31.21/month

I went a little over my entertainment budget, but I don’t regret it. This quarter it included taking my partner to a spa to help with his stress, watching several $6 AMC movies (it’s $6 every day before 12pm!) and going to karaoke. I ended up seeing Avengers: Endgame (spoiler free review below) and The Hustle (which was surprisingly funny despite the low Rotten Tomatoes’ score). The only recurring expense in this category is our Netflix subscription that we allow approximately 20 other people to use for free…maybe I should move that to the Giving category…

VACATION – $161/MONTH

Vacation Spending – $93.14/month

June marked the beginning of camping season! We camped near the base of the active volcano Mt. St. Helens and had an awesome, relaxing time. Camping is such great frugal fun. I also was surprisingly spontaneous (I love my lists and planning things months in advance to the great chagrin of some friends…) and agreed to go to a house on Lake Chelan to work for July 4th week – I’m actually writing this while looking at the water right now! Check out my Instagram to see pictures.

Travel – $27.25/month

This category also includes taxes for all my remaining flights this year, which I travel hacked! I’ll be detailing how many points I spent and how much I saved in my usual annual Travel Hacking post, but in summary, I booked free flights to Atlanta to work from home for 3 weeks this summer and back to Atlanta to work from there for 4 weeks during Christmas as well as a week at FINCON! It’ll be my first official personal finance event and my first conference ever – I hope to see y’all there!

Friends Visiting – $41.23/month

In addition to all those fun times, my partner’s parents, his sister and my Mom visited this quarter, which explains my “Friends Visiting” category explosion. I have this separate category because it shows me on average how much extra I spend with certain friends and family so I can budget accordingly for their next visit (Nerd Alert!)

LONGTERM – $134/MONTH

This category is for you guessed it “longterm” items that come up rarely.

This quarter I paid the $95 annual credit card fee for my Chase Sapphire Preferred. I’ve had it for 4 years and every year it’s paid for its annual fee and then some by saving my ass and reducing my stress. The latest butt saving event occurred on our way back from Costa Rica:

OVERALL

And that’s it for this quarter! So far this year I’ve spent $9,114.65, 48% of my $18,727 goal. That’s perfect! I’m projected to spend $18,229.30 in 2019, which is on track with my goals while living a lavish life. To the rest of 2019!

How has your spending been lately? Are you on track to reach your annual goals?

Wow, rent in Seattle is more than Tokyo (I am assuming you split it with your partner). But amazing job, your budget clearly shows what you value in life 💚

IT IS?! Wow – I’ve only heard in conversation, but I thought Tokyo would be a lot more. How much is typical rent there? Our rent here is actually low for near downtown. And yes I split with my partner 🙂 .

Spontaneous camping… I don’t know if I believe it 😉

Considering we hang out as much as we do, I’m in awe of your low spending. Though I guess my spending is really 3X plus one very expensive dog. Gulp.

Lol – the spontaneous part was the last minute lake house with Julie. Spontaneous camping is still not in my wheelhouse 🙂 . And haha yeah I think we’re on the same track if your spending accounts for the extra people and animals in your house 😉 .

Wow, your food bill is really low. If there is a competition, you’d probably win this category. Especially if you can keep the alcohol to $0 like in June. 😀

Haha – thank you? In my groceries post that I linked above I had all kinds of caveats like how many calories I require (less than a tall man for example) and what I eat is fairly cheap (fresh meat and veggies vs packaged stuff, which is fairly cheap). Maybe I should make myself a medal 😉 .

you gotta have a strong plunger. see my last post about misadventures in plumbing!

have fun at the fin-con. we’ll be in our wilderness cabin rental that week. i haven’t done as much sous-vide this year but it’s coming soon. we spent a lot on our house this year, but the rest of the year should be light.

Haha I’ll check it out over lunch. And agreed on a strong plunger. Our previous one must have been designed by someone who has never designed anything before because it was straight up silly. Have fun at your cabin! That sounds relaxing. I will do my best to have fun at FinCon! Right now I’m just trying to figure out how I’ll be around so many people for a solid week without needing a month to recover. Woohoo on more sous vide! Let me know how it goes. We’re always looking for more recipes. And fingers crossed the rest of the year will be light on house expenses!

We are tracking pretty closely! I’ve spent $9,657 so far this year.

It’s fun to do a half-year check-in to see how it’s all going. Our rent is about to go from $930 to $500, so I’m excited for the savings from that! Although next year it is bound to skyrocket again when we move to Santa Barbara.

I love seeing everything you’re doing without spending a ton, and to have a spending twin 🙂

Woohoo twins!! Apparently my stepdad was freaking out today after reading this and my Mom had to talk him down LOL. If he starts up again I’ll point him to your blog so he can see I’m not out of my mind 🙂 and it’s totally possible to live an awesome life in the PNW on not that much money. And $930 rent is amazing, but $500 for the whole place = WOAH! How much is rent in Santa Barbara? I’m sure y’all will find a way to get a good deal! So glad you enjoyed the post 🙂 .

Excellent work on the budget! I’m going to have to dig in a bit more to the post on how you handle your food costs. I think we spent that much last month just on fresh berries. 😂

Thank you! And haha yeah definitely check out my grocery post below. I also love berries and fruit, but I only buy them when they’re on sale 😉 – which explains why I bought 10 lbs of grapes in the last 2 weeks….

https://apurplelife.com/2019/01/15/how-i-spend-125-a-month-on-groceries/

Impressive! And now I am hungry for fajitas!! Those look so good!

Thank you! And ugh fajitas – ME TOO! I can confirm they were delicious 😉

My spending has been a little higher than I’d like, but at the same time I’m trying to balance quality of life and frugality. So I go back and forth on how much I care about weekly takeout. I hope to have a firmer idea soon of where my priorities lie.

The Republic Wireless deal sounds awesome. Not enough to get me to switch to a phone with an Android OS — tried it Android once on a tablet and once on a phone and never found it to my liking — but awesome for anyone who ISN’T too dunce-y to work with Android. I’m thinking I’ll switch to Mint soon to cut my phone bill about in half to $15 a month. So that’ll be nice.

I’m with you – it’s all about balance. Take out is totally worth it sometimes! And yeah Republic Wireless is awesome, but definitely not for non-Android peeps 🙂 . Mint sounds really cool though! I only heard of them recently. Good luck with the switch!

Firstly, that food looks delicious. Secondly, whats your strategy for accumulating all those points on your CC, which bought you that stress-reliever on the way back from Costa Rica? Congrats on keeping such a smart budget.

Haha – glad you think so! I can confirm it was yummy. As for the credit card, I don’t have a strategy. They have travel insurance that includes trip delay insurance built in as a perk of the card so if I’m delayed a certain amount of time they’ll reimburse me for any hotel, taxis, and food I consume during the delay – I believe it’s up to $500 an incident. It’s an amazing perk and that’s what’s saved my butt and stress levels all these times. And thank you!

I’m impressed with your super low grocery spending. We easily spend over that amount whenever we go to Costco.

Thank you! I’m curious what you buy from Costco to spend more than that and wonder if it’s just giant amounts of food that actually lasts multiple months 🙂 .

How do you spend so little? I am so impressed by it but I can’t wrap my head around how do it. I have relatively low living expenses and I created a budget a few years ago and have been tracking my spending but often go over my weekly budget (which is $250!) and often have extra stuff on credit cards to pay off (I never pay interest on any of it because of how I work it but still). I am trying to get a hold of my spending and ramp up my savings as much as possible but it seems impossible to be able to do that without saying no to everything. I even work Instacart to make extra money on top of my full time job. What surprises me the most is what you spend with friends in town. If i have friends come visit me in LA I spend at least an extra $100, if not more, than my weekly budget. How do you manage it? What does your social life look like on a week to week basis?

I think it’s because I don’t have the items that take up most people (like parents’) budgets: no house, no car, no kids, no pets (and so no insurance for those items).

I’d love to hear more about your situation if you’re willing to share to see if there IS anything to cut. It’s also possible there isn’t. It’s my opinion that you shouldn’t have to say no to anything you actually want to do while following your budget – I don’t.

As for friends coming to town the extra money I spend is for more eating out and drinking out then usual and cars to get around since it’s more cost effective than public transit if there are a lot of us. I think LA is more expensive than Seattle in that way and definitely on the lack of public transit/wild traffic so ride shares are expensive side of things.

As for my general social life, I think I’m lucky because the things I like doing with friends are low cost or free. We have a weekly Supper club where we cook for everyone, talk, share wine and usually watch a show or movie on Netflix or that we rent for $5 after. I also have friends over to play video games – and sometimes stream them. We go on long walks and chill in parks. I do often also meet them for drinks or dinner or even vacation – this past weekend we went camping and it was about $100 a person for everything. My social life is full – sometimes too full 🙂 . What kind of activities do y’all usually do together?

My bills aren’t crazy, my rent is $642 (going up this month from $600). Gas is ~$6/month, Power ~$40/month, Cable ~$40/month, Internet $22.67/month, cell phone $77/month, renters ins is $5.50/month. I could cut out cable but I split it with my boyfriend and our roommate so they would have to be on board with getting rid of it as well. Cell phone could prob be reduced but I don’t know if I can use an Android or other type of phone, and its not too crazy for an unlimited plan.

I did lease a car recently since my car (that was paid off) started to give me issues. They wanted me to put in over $2000 in repairs in a car not worth more than $4000. But a lease wasn’t smart either but i didn’t have another option since I don’t have significant savings outside of my retirement accounts. So that’s $332 per month I am stuck with for 3 years. Car insurance is $115 and I shopped around quite a bit before committing.

I also have a pet and recently got insurance for her because i see how much they can cost as they get older. Right now it is around $82 per month but I’m up for renewal and will call to get that reduced in the next few days.

I think my day to day spending is what gets me. My friends and I don’t do a lot of free or inexpensive things. We used to go out to bars every friday and saturday night. I would spend anywhere from $50-$75 per night this way. We have slowed down on going out since we have gotten older but even now still if we go to brunch it turns into a whole day of bar hopping. Also, everyone is turning 30 this year and so we take weekend trips to different places and rent out an Airbnb. These typically cost around$150 per person for the weekend and includes some food and drinks but not all. I’ve already had 5 trips like this this year and 3 more coming up.

When I made my budget I thought $250 a week would be enough to include everything I need but it usually isn’t, especially when I’m traveling. I’m starting to analyze on a monthly basis where my moneys goes and it looks like eating out is my biggest drainer but I don’t feel like I eat out that often! I’m getting better at prioritizing things and saying no to things that don’t line up with my budget but I get a lot of pressure or guilt from my friends when I do and I can’t figure out how to balance it all. One of my best friends and I even got into a huge fight a while ago when she felt like I was neglecting our friendship bc I was saying no to going out and spending money. It was hard for her to understand where I was coming from 🙁

I appreciate your response! And love your blog! Any suggestions are greatly welcomed!

So adding up all the expenses you listed (even assuming you pay for all the cable and internet which I believe you split with your roommates) you spend less than me so it sounds like the things you need to reign in are exactly what you identified: Everything else 🙂 (drinking out, eating out etc).

I feel lucky that I don’t enjoy bars or hop hopping for more than 1-3 drinks. After that we go to a friend’s house or terrace or roof deck and chill with cheaper drinks there if we want to keep the party going. Same with brunch. Is that something you would enjoy and could do?

Similar thinking for these trips – I go on about 6 camping trips a year as I mentioned and they cost similar to your weekends away – and that’s on top of my international and domestic travels. I doubt those mini-vacations of yours are what’s breaking the bank – it really does sound like your day to day spending is doing it.

I’m sorry about your friends pressuring and guilting you – that sounds hard…and weird if I’m honest. Even when I lived in Manhattan and drinking out and spending money are the go to past times no one gave me shit for suggesting an alternative to a spendy activity I didn’t really want to do. It didn’t always work and sometimes I ended up doing the spendy activity to be with them, but usually it did. I still got to be with friends and didn’t spend that much.

Thanks so much! Glad you like the blog. If you want to get into a more in-depth discussion about this feel free to email me: apurplelifeblog [at] gmail.com

I’m impressed by your low grocery spending – mine is higher but I’m OK with that. I started saving a lot of money when I switched over to ALDI a few years back, with some farmers market purchases thrown in there. I’m spending a lot less now that I am not lifting heavy (daily calisthenics instead, oddly I’m looking more muscular than when lifting), so that’s helped. Otherwise my spending looks pretty similar!

I switched over to Ting after sharing a family plan with my sis and her fam – even as an add on I’m paying about half, and I was able to use my iPhone too, which was nice. I like that you only pay for what you use – my bill so far, with 8 days to go, is $19.

Super cool! Sounds like you’ve found a great balance for yourself. Ting sounds interesting – I’ll add them to my research list! Thank you for stopping by.

It seems like the only annual credit card fee you report is the $95 Chase Sapphire Preferred. How do you travel hack without incurring additional annual fees? Are you getting new no annual fee cards (despite the lower sign up bonus)? Or are you canceling new cards within a year to avoid the (majority of a) fee?

Hi There – I don’t use the Chase Sapphire to travel hack. The reason I keep it is as travel insurance and every year I’ve had it so far it’s paid for its fee and then some by paying for last minute hotels and meals when I’m stranded somewhere overnight. For travel hacking I get cards that have no fee the first year and then cancel before the annual fee is charged for the next year. Happy to answer any more questions you have!

Aha! So you rack up points on the other cards, but when it comes time to actually pay for the taxes/fees on the flight you use the Chase card to get trip insurance? (I am new to the travel hacking concept, and I honestly don’t fly or plan to fly that much , so I want to make sure I’m going to do this in a smart way!)

That’s exactly correct yep! Also if it’s a better deal to just buy the flight in cash (instead of use points) I buy it with my Chase card.