This is only my second time writing a post like this. In retirement I’ve posted about my spending, my income and that’s basically it.

But I wanted a place to talk about my money moves in general and sum everything up for the year, so that’s what this new annual post is. So let’s look at my overall financial picture and see what the future holds!

Income & Spending

2025 Spending: $35,950

2025 Profit: $7,553

I’ve already written entire posts detailing my spending and income in 2025 in the links above. This year, I spent $35,950, which is over the $24,000 I budgeted for this year. However, that was for good reason, which I detailed in the posts below. And the $7,553 was a pleasant surprise that my pessimistic brain doesn’t think will continue 🙂 .

- I Got A Homebase! (But Will Still Travel 1/3 Of The Year)

- I Bought A Car! What I Learned As A First-Time Car Buyer

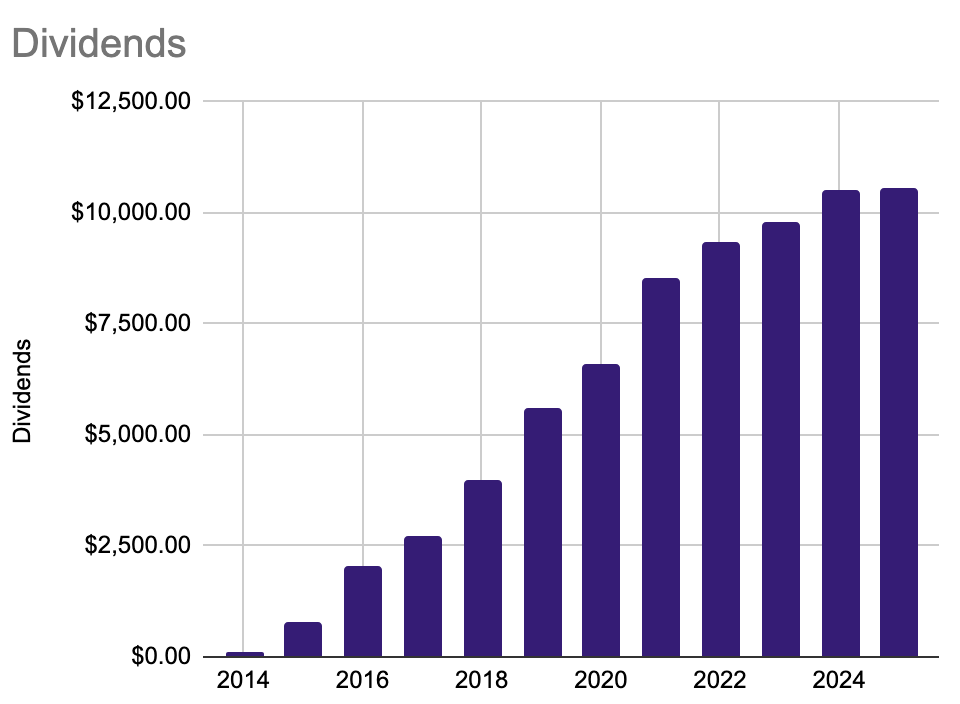

Dividends

2025 Total: $10,577.73

Of that, I received $4,098.43 of dividends in my checking account from my Taxable Brokerage this year. The remaining dividends were automatically reinvested into my Traditional IRA and Roth IRA accounts. And here’s how my dividends have grown since I started investing intentionally:

Retirement Withdrawal

2025 Withdrawal: $20,000

Just like previous years, this year I withdrew $20K from my Taxable Brokerage account. It’s a pretty straightforward process that I detailed in this post:

Roth IRA Conversion Ladder

2025 Conversion: $0

Similarly, my roth conversion is an annual activity that’s not a complicated process since I’m now used to it. The only challenge is that I have to wait until the last few days of the year to estimate all of my income and figure out how much I can convert from my Traditional IRA to my Roth IRA tax-free.

However, I didn’t do a roth conversion this year. That’s because moving my state of residence from Washington to NY State, being a part of the ACA Marketplaces in both states and having more complicated taxes as a result made me want to lean on the side of caution.

- I Became A NY Resident (Again): Real ID, Voting, Libraries, Healthcare and Taxes

- I Joined The Health Insurance Marketplace

So I’m not doing a conversion this year. Once I see what my approved tax forms look like in 2025 across those two states as well as federally I’ll make a plan for how much I want to convert in 2026. I previously detailed how I figure all that out and make the conversion in a post here:

New York State Investment Taxes

2025 Estimated Taxes: -$880

Federal taxes on my investments are still $0 like I’ve kept them for all of my retirement. However, the state I decided to have a homebase in (New York), counts investment income as regular income and taxes it as such. This is obviously a fine price to pay to be near my family and maintain the roads I’m driving on and the other services I enjoy often, such as the local library.

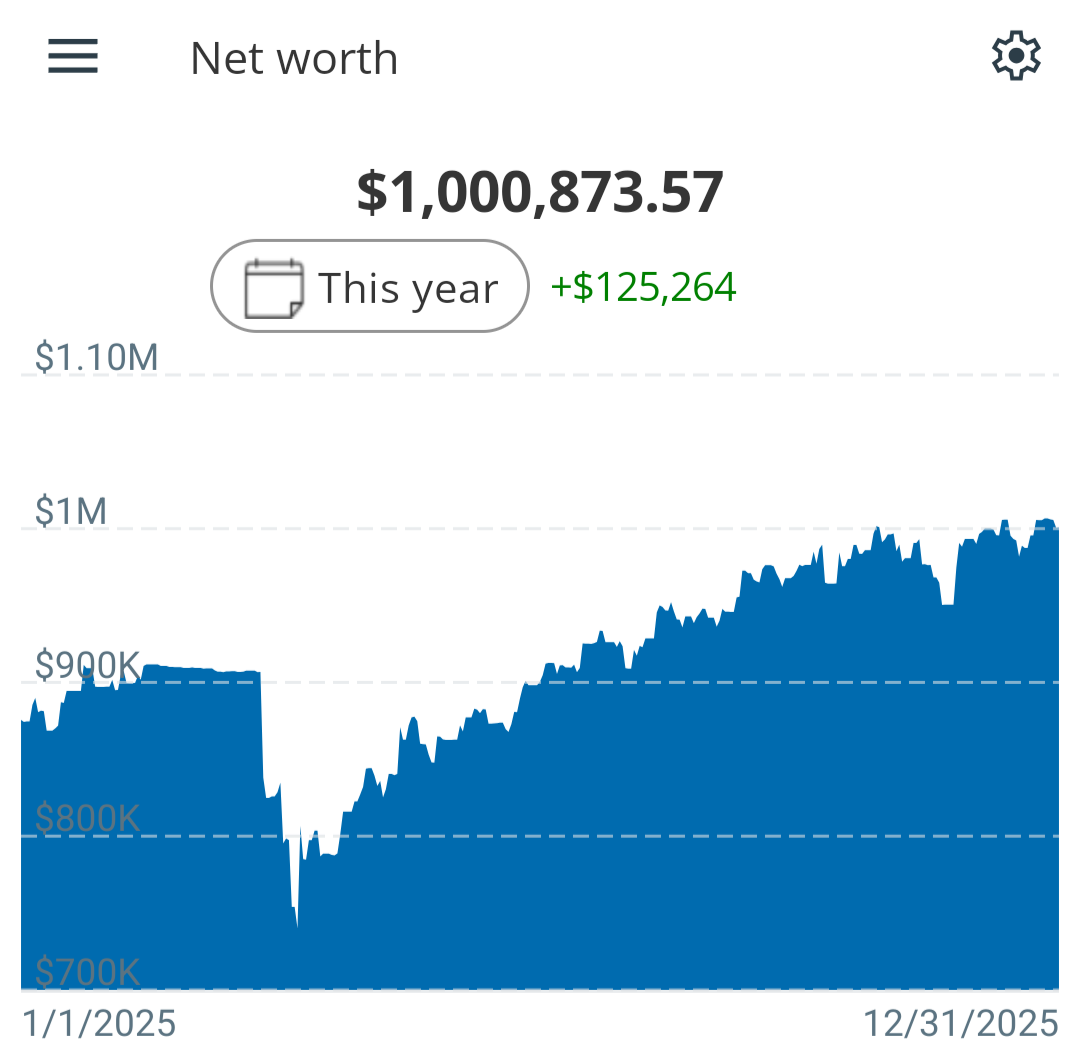

Net Worth

2025 Net Worth: $1,000,873

WOW!!! That’s a 13% increase in 2025. Also, this is the year I became a Millionaire 🙂 .

Since October 1, 2020 (the day I retired) my net worth rose $460,873 or 85%. I must admit that this was not the financial outcome I was expecting when retiring into a pandemic and possible recession, but here we are 🙂 . Another lesson is that I cannot predict the future and should never try!

I update my net worth on Instagram and The Numbers page every month so check that out if it’s something that interests you. It’s been fun to watch and absolutely wild to see the power of compound interest in action.

As a reminder, my investment portfolio is 100% VTSAX and I wrote about why in detail below. The TL;DL is that I can easily weather the downsides and it’s just simpler (no rebalancing or tax optimization for where I put stocks and bonds).

In case you missed it, here is how I manage my money:

And here’s how my net worth currently breaks down across my accounts:

Cash: $48,149.04

Taxable: $360,965.98

Trad IRA: $454,206.79

Roth IRA: $114,624.38

HSA: $22,927.38

To see how far I’ve come – below is my net worth since I entered the workforce in 2011. Not bad 😉 .

2026

Spending Goal: $25,000

In 2026 I’m going to continue my trend of increasing my spending goal to include inflation. 2025 saw 3% inflation so my spending goal for 2025 will be $25,000. And because I’m me, I already have most of next year’s travel adventures planned out in my head 😉 . Spoiler: 🇲🇽 and 🇪🇨.

Conclusion

And that’s what my money was up to in 2025! Overall I’m in awe of the power of compound interest. It’s one thing to read about compounding and another to see it in action and I’m very excited to see what happens next 🙂 .

I’m happy for you Purple, it’s amazing to see this progress. Interesting that your money is working now harder than you possibly could! The 8th wonder indeed.

Thank you so much! That’s a great way to look at it and yeah it’s absolutely wild 🙂 .

You have a pretty large cash stockpile relative to your total net worth. Is that how much you always hold, or are you keeping more cash on hand as a recession hedge?

I know no one can time the market, but valuations seem ridiculously high right now. That’s very nice for those of us that own stocks, for sure, but I wonder if I should sell a little more than I usually would and lock in some gains now, while times are good.

I would say 2 years of expenses in cash in retirement is at the low end of recommendations. Totally different when you are still in the accumulation phase, but Purple is in retirement, so 2-5 years in very low risk assets (cash or cash-like investments) is standard advice.

Congrats on becoming a millionaire Purple!! You are doing such awesome work both in investing but also in showing what real life can throw at you in retirement. Thanks!

What would you do with the money after selling?

I usually only keep the cash for my next 12 months’ expenses ($25K) and this is an accidental amount of extra cash. It piled up from accidental income the last few years in addition to my dividends and continuing to withdraw $20K/year. I thought about not withdrawing this year since I had so much cash, but decided to withdraw anyway.

The additional cash isn’t a recession hedge, but a “homebase” hedge since I have an apartment and a car now that might need an influx of cash randomly and I don’t want to have to think about cash flow in those moments. All that to say: you do you 🙂 .

Congrats on hitting the $1M mark! I already teased you about this on Insta, but in just a few years you will be a Female Black Multimillionaire.

After taking a two year cooling off period to think about it, I finally retired this year! I can’t say enough about how good it is, and I’m only two months in. I’m so busy that I don’t see how I ever made time for work.

Thank you Birchie! And haha yeah the countdown has begun 😉 . CONGRATULATIONS on your retirement!!! I’m so happy to hear you’re enjoying it and already are having that classic retiree thought. I love it 🙂 .

Love the detail, as always, and the progression still takes me by surprise. You don’t add to your investments each year, right? Compound interest really is the eighth wonder of the world.

Thanks! And yeah I haven’t added anything since I quit my job.

Happy New Year, and well done in 2025. Welcome to the millionairs club! Amazing eh, that money keeps making money. And if we are financially not making any big mistakes, life becaume quite easy (from the money side at least). Looking foward to following your journey in 2026. Take care

HNY and thank you! That’s so very true 🙂 .

All set up with an ACA plan now. I think I’m going to toggle off the reinvestment of taxable brokerage dividends soon. Thanks for all of the great ideas!

Woohoo!!! So happy to help 🙂 .

Congratulations Purple on a great 2025! You are a great example of when you create a strategy and plan and stick to it, monitor and adjust accordingly, it really works. I hope more people share your blogs as I do with the people in their lives so that they can learn from your experience. You are making a difference by being generous in sharing your knowledge and learnings along the way.

Thank you so much BreCam! That’s so kind of you to say 🙂 .

Your journey is impressive. Your asset mix is right on! Have you thought about how you might handle a 5 year decline in the value of your investments or a collapse of the value of the US dollar? Congrats on your first million!

Thanks! For a 5 year decline I’d do the same thing as any major decline (more than a 50% stock market decrease) – spend less (most of my spending is discretionary so that’s easy to cut down on) and withdrawal less from my investments. As for the US dollar, it’s already been declining and we’re still traveling internationally so I would probably just continue that or maybe travel less and use that homebase I’m also paying for lol.

Congrats on hitting millionaire $tatu$! 😀

For real, I think that’s a much harder bar to clear when it’s all liquid, as your Instagram post mentioned. People who buy a house have a lot of money tied up in that property, and associated furnishings/taxes/repairs provide an ongoing drain on cash reserves. So in your case, since that amount is liquid, you can keep getting those sweet, sweet dividends!!!

Also, the markets have been totally wild lately. Gold, silver, bonds, US stocks, and international stocks all sometimes go up or down at the same time. I wish I could explain what’s going on there…

Thank you! And yeah the markets are wild.